For residents of the Pacific Northwest, state level “death taxes” can be a significant hurdle to overcome. While both Oregon and Washington impose an estate tax, their rules, exemptions, and rates have diverged significantly as of 2026. Understanding these differences may be important for ensuring your assets reach your beneficiaries rather than the state treasury.

At a Glance: Oregon vs. Washington Estate Tax (2026)

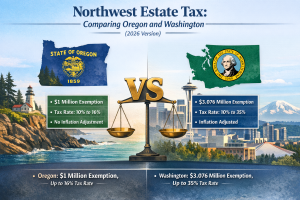

| Feature | Oregon | Washington |

| 2026 Exemption | $1 million | $3.076 million |

| Tax Rates | 10% to 16% | 10% to 35% |

| Inflation Indexed | No | Yes (starting January 2026) |

| Top Rate Threshold | $9.5 million | $9 million |

| Spousal Portability | No | No |

Oregon: The Nation’s Lowest Threshold

Oregon remains home to the lowest estate tax exemption in the United States, fixed at $1 million.

- Static Exemption: Unlike many other states, Oregon’s $1 million threshold is not adjusted for inflation. This leads to “bracket creep” as home values and retirement accounts grow.

- Tax Brackets: The Oregon estate tax is progressive, starting at 10% for the first dollar over $1 million and topping out at 16% for estates over $9.5 million.

- Legislative Update: Recent proposals (such as Oregon Senate Bill 1511 in 2026) have aimed to raise Oregon’s estate tax exemption. However, such proposals have so far failed to pass.

Washington: High Exemption – High Stakes

Washington recently overhauled its estate tax system, resulting in a higher estate tax exemption, but also the highest top rate in the country.

- 2026 Exemption: For deaths occurring in 2026, the exemption in Washington is $3.076 million. This exemption is now indexed on an annual basis to the consumer price index (CPI) to adjust for inflation.

- Aggressive Rates: In July of 2025, Washington increased its top marginal rate from 20% to 35% for taxable estates exceeding a gross estate value of $9.5 million.

- Business Relief: Washington offers a generous qualified family-owned business deduction, which has also been increased to $3.076 million for 2026.

Key Planning Considerations

- Cross Over Point. Analysis suggests that for estates valued below approximately $7.5 million, Washington’s higher exemption makes it a more estate tax-friendly environment. However, for estates above this threshold, Washington 35% top rate may result in a higher total tax bill than Oregon’s 16% maximum rate.

- No Portability. Neither Washington nor Oregon allows for estate tax exemption portability, meaning if one spouse dies without using his or her exemption, it is lost. This makes use of credit shelter trusts essential for married couples to maximize both spouse’s individual exemptions.

- Non-Resident Exposure. If you live in a state like California or Florida, but own real property in Oregon or Washington, your estate may still owe taxes based on the value of the in-state property.